-

Celebrate Sangeetha's 52nd Anniversary Sale Win a Gold Coin & Get Assured Vouchers worth Rs.60,000*

-

Heading - Introducing Vivo X300 Series Own the latest Vivo X300 Series with HDBFS

-

The Summer of Chill Cashback Upto ₹31,000* + Scratch & Get an Exciting Reward!

-

Introducing Samsung Galaxy A57 & A37 5GEMI Starts at Rs.1,750*

-

Join the celebration with HDBFS Car Loan + enjoy Assured Vouchers worth upto Rs.60,000*

-

Instant Personal Loan Get an Instant Personal Loan now for upto Rs. 25 Lakhs!

-

Instant Pre-approved Offers Apply for Pre-approved loans in just 5 mins with Zero documentation!

-

HDB ontheGo App One application to view & manage your loan account & also apply for new loan

-

Celebrate Sangeetha's 52nd Anniversary Sale Win a Gold Coin & Get Assured Vouchers worth Rs.60,000*

-

Heading - Introducing Vivo X300 Series Own the latest Vivo X300 Series with HDBFS

-

The Summer of Chill Cashback Upto ₹31,000* + Scratch & Get an Exciting Reward!

-

Introducing Samsung Galaxy A57 & A37 5GEMI Starts at Rs.1,750*

-

Join the celebration with HDBFS Car Loan + enjoy Assured Vouchers worth upto Rs.60,000*

-

Cashback offers on Iphone17 Pro Cashback offers upto Rs. 5,100*

-

Instant Personal Loan Get an Instant Personal Loan now for upto Rs. 25 Lakhs!

-

Instant Pre-approved Offers Apply for Pre-approved loans in just 5 mins with Zero documentation!

-

HDB ontheGo App One application to view & manage your loan account & also apply for new loan

- Home

-

About Us

-

Products

- Hot Offers NEW

- Blogs

-

Investors

-

Customer Services

- Careers

-

CSR

Call Us

+91 44 42984541(Charges Applied)10.00am-6.00pm, Mon-Fri (Excluding Holidays)

Follow Us

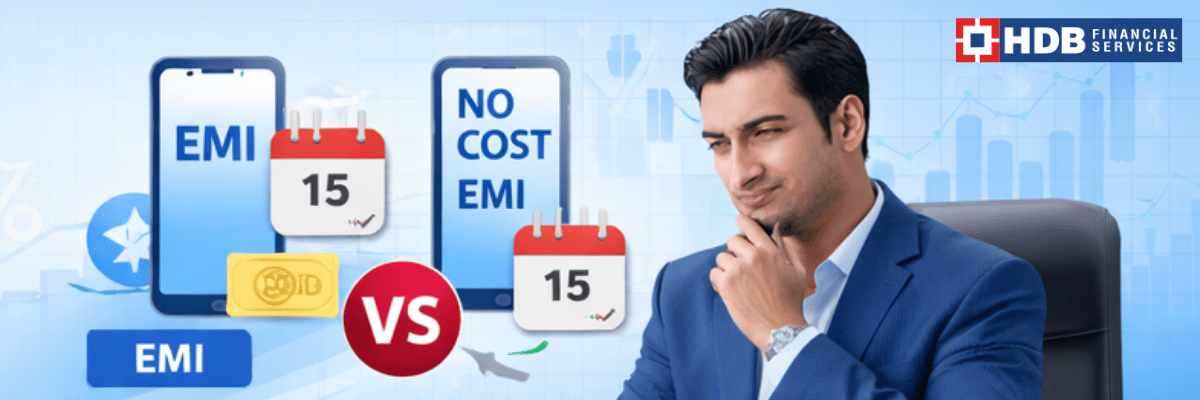

EMI vs No Cost EMI - Understanding the Difference When Buying Phones

2026-03-26

EMI vs No Cost EMI - Understanding the Difference When Buying Phones

EMI and no-cost EMI are popular payment options available to consumers and their popularity in the smartphone market has only increased. In 2024, the Indian smartphone market grew by 4%. No-cost EMI schemes were the most popular financing options in the mid-range and premium segments. This means that they made higher-priced devices more accessible. While buying a mobile phone on no-cost EMI promises zero interest, you must scrutinize the terms for hidden fees or discounts and understand the finer details to make informed purchasing decisions.

What is EMI?

An Equated Monthly Installment (EMI) is a fixed payment that a borrower makes to a lender each month. This covers both principal and interest, making sure that the loan is fully repaid over a set period.

EMI amounts are calculated using the formula:

EMI = P * [( r * (1 + r)^n)) / ((1 + r)^n - 1)]

where

P = Principal amount borrowed

r = Periodic monthly interest rate

n = Total number of monthly payments

What is No Cost EMI?

No Cost EMI is a financing option where the buyers pay for the products in equal monthly installments but without any explicit interest charges. What happens in practice is that the seller or the lender neutralizes the interest. They do this by not offering discounts or by including the interest in the product’s price itself.

For example, this is a breakdown of a smartphone bought on regular EMI:

Price of the smartphone - ₹50,000

Rate- 12% per annum

Tenure- 12 months

Total price to be paid- ₹53,316

Monthly EMI- ₹4,443

Here, you're paying ₹3,316 extra over the year as interest.

If the same smartphone was bought at No Cost EMI, the total price would be ₹50,000 over the same period and with no extra interest. The monthly EMI would be ₹4,167 and the price of the product stays the same with no extra charges or hidden interest.

However, sometimes, the interest is hidden. A ₹15,000 phone may be sold at ₹17,000 under No Cost EMI by covering the lender’s cost. This structure is very popular for electronics and high-value items.

Differences Between EMI and No Cost EMI

Hidden Costs and Fine Print

The processing fees and GST at 18% are common, even in no-cost EMI offers, but the hidden costs can increase the total amount that consumers and businesses have to pay. The RBI has said that zero percent interest is just a marketing term that sellers use. In reality, the interest is already embedded in the product’s price or neutralized by removing the discounts. Additionally, if the buyer misses an EMI payment, they can attract late fees that exceed 24% per annum. This will lower their credit scores, and the entire amount will be counted against their credit limit.

When Should You Choose EMI?

Choosing between EMI and full payment depends on how tight your cash flow is, whether funding is available, and what best value can be offered. A regular EMI is a good choice if you want to purchase from a broader range of electronic products. The only downside is that it increases the total cost of the purchase due to the interest, which is in the range of 16% and 24% for electronic items. However, avoid both options if you can make the payment upfront or if the hidden costs outweigh the benefits.

Data and Trends

Installment-based purchases, especially EMI and no-cost EMI, have grown significantly in India’s smartphone and electronics market. During Amazon’s Great Indian Festival 2023, one in four purchases were made on EMI, and 75% (three-quarters) of these EMI transactions were on no-cost EMI. Amazon also reported that 2.5x more premium smartphones were sold compared to the previous year.

Practical Tips for Buyers

When weighing EMI offers for mobile phones, you should carefully evaluate the total cost, eligibility, and terms to avoid making irreversible mistakes. Always compare the EMI price with the regular cash price, review the processing fees, GST, and tenure options. Also, use tools such as Credit EMI/No Cost EMI Cost calculators so you don’t make any errors. Go over the terms carefully to protect your finances.

Conclusion

EMI and no-cost EMI options have transformed consumer purchasing behavior, especially for high-value items such as smartphones. The main difference between the two is that regular EMI adds interest and fees, which increases the total outlay. No-cost EMI spreads payments at the listed price but hides the costs in processing fees. So, before committing, compare the total costs, scrutinize the terms, and make sure that your choice aligns with your cash flow and procurement policies.